What if an AI company "solves" Insurance?

No company is an island, entire of itself

Disclaimer: The views and opinions expressed in this blog are entirely my own and do not necessarily reflect the views of my current or any previous employer. This blog may also contain links to other websites or resources. I am not responsible for the content on those external sites or any changes that may occur after the publication of my posts.

End Disclaimer

“send not to know for whom the bell tolls, it tolls for thee” -John Donne, Meditation XVII

"Ask not for whom the bell tolls; it tolls for thee" -Ernest Hemingway, For Whom the Bell Tolls

“Time marches on. “ -Metallica, For Whom the Bell Tolls

Note: This post is Insurance and Reinsurance Industry specific, because that’s where I work now, but this idea applies to all industries.

So wherever you see the words “insurance” or “reinsurance”, copy paste your own job or industry.

I thank you.

So, maybe someone else figures out how to apply AI in the (re)insurance industry and completely disrupts the industry - puts a ton of people out of work.

Google? Amazon? Citadel? Palantir? RenTech? Someone we haven’t heard from yet? Some company that doesn’t yet exist?

In a recent CNBC interview, a tech company CTO said that his firm completely automated an insurer’s underwriting- took it down from 2 weeks to 3 hours.

Lots of immediate questions: One line, all lines? Better underwriting, worse underwriting? No touch, some touch? Do you have historical results good enough to train a new model on? What senior underwriter is going to hand over their decisions to an algorithm? I haven’t met a single one who would do that.

If this is true- wow, that would require a (re)insurer to have high quality, standardized data across lines. I haven’t met one that has that.

So this proclamation doesn’t really pass the initial first whiff smell test…

But…

It’s definitely coming.

From someone.

So far, when some tech third party has come to me and said, more or less, “we solved it”- solved for claims, solved for underwriting, solved for insurance, they bring with them a highly curated demo that can’t handle edge cases and a sometimes debatable amount of AI (offshore humans). Or, they ask you to “work with them” in hopes that they can literally build the product while using your company as a guinea pig.

The current and near future llm technology is getting such that we are closer to “solving” for many llm+AI vision automation tasks. Data ingestion automation. Not 100% ( I see you mechanical turk), but closer to a tenable working solution in pockets and certain lines of business.

In addition, the component pieces are coming together for certain lines where you can start to see what an “end to end “ algorithmic solution looks like.

But, as I’m sometimes reminded, (re)insurance is a staid, heavily regulated business. We sleep safe at night in the comfort that no one would bother to disrupt the industry.

“This is a gentleman’s game” someone told me when I first got into the industry.

Holy smokes.

I had just come from the hedge fund industry, where people would pry single-digit basis points from the still-warm hands of their slain competitors, so this statement came as a shock to me.

The game theoretic implied in the “gentleman’s game” comment relies on maintaining an agreed upon “disruption detente” a semi-stable equilibrium where no player will unilaterally improve their position by changing strategy.

That’s not life.

Everything remains a “gentleman’s game” until it isn’t:

Retail

Disruptor: E-commerce (Amazon, Alibaba)

Impact: Closure of many brick-and-mortar stores, especially department stores and malls. Significant job losses in traditional retail roles.

Manufacturing

Disruptor: Automation and robotics

Impact: Massive reduction in factory jobs, particularly in developed countries.

Media and Publishing

Disruptor: Digital media and online content platforms

Impact: Decline of print newspapers and magazines, job losses in traditional journalism and printing.

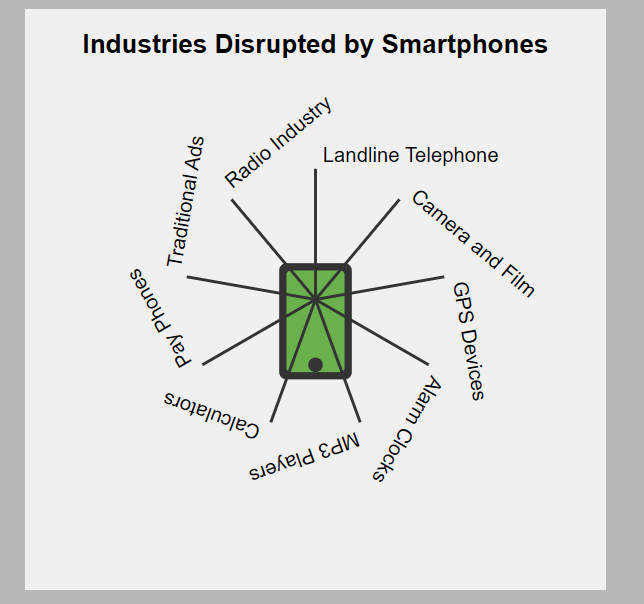

Photography

Disruptor: Digital cameras and smartphones

Impact: Near extinction of film processing jobs and traditional photo studios.

Music Industry

Disruptor: Digital streaming (Spotify, Apple Music)

Impact: Decline of physical music sales, affecting music stores and distribution jobs.

Video Rental

Disruptor: Streaming services (Netflix, Hulu)

Impact: Extinction of video rental stores and associated jobs.

Travel Agencies

Disruptor: Online booking platforms (Expedia, Booking.com)

Impact: Significant reduction in traditional travel agent jobs.

Banking

Disruptor: Online and mobile banking

Impact: Closure of physical bank branches, reducing teller and other in-person banking jobs.

Telecommunications

Disruptor: Voice over IP (VoIP) and mobile technology

Impact: Decline in landline-related jobs and traditional telecom infrastructure roles.

Postal Services

Disruptor: Email and digital communication

Impact: Reduction in mail sorting and delivery jobs.

(Re)Insurance

Disruptor: A big tech/AI company, quant hedge fund, someone else

Impact: Decline in (re)insurance jobs across the board. Significant reduction or Extinction in certain areas

Consider the destruction that smartphones hath wrought across these industries:

Decline, significant reduction, extinction.

What can a company do to stop, prevent, or ameliorate this kind of disruption?

Well:

You can’t stop it.

You can’t prevent it.

But you can try to help make it a landing that people can walk away from.

If some other company “solves for” insurance completely, including the “everyone has bad data” part:

Short term outcomes could include:

Looking like how Bloomberg terminals are used in finance- table stakes to compete, everyone needs to use them, high price inelasticity.

Or…

Several initial adopters of said “3rd party” beating the market with a new algorithm or tech. Alpha has a half life- would this be temporary?

Longer term outcomes could include:

Industry consolidation as smaller players unable to compete are acquired or go out of business.

“3rd party company” becomes a de facto standard, potentially raising antitrust concerns.

Increased barriers to entry for new insurers without access to the “3rd party company’s” technology.

How to prepare for a third party AI disruption?

For the C-Suite executive(s) (CEO/CFO/COO) in charge of fending off technological disruption and futureproofing, I offer you a kind of abridged si vis pacem, para bellum checklist:

Clean your data- Yes, this one again. Start with a single line of business and build out. If a disrupter offers new tech, the tech needs to work on something. AI feeds on data.

Build a data strategy-AI feeds on data- decide on a methodology- centralized vs decentralized, who owns what, or nobody owns anything. People are incredibly protective of “their data”. Without a plan, a lot of time can be wasted extricating data out from their fiefdoms.

Grow/hire an ml team- Don’t cobble together a Frankensytem from multiple vendors. Hire a team that has shown practical evidence of building both discriminative and generative models. To quote Henry Ford, “If you need a machine and don't buy it, then you will ultimately find that you have paid for it and don't have it.”

Pop quiz hotshot (Dennis Hopper, Speed): You have a data set with 100 samples, 95 are false, 5 are positive. You predict false and get a 95% accuracy score- Is this great, good, terrible? Or entirely the wrong metric to use with an imbalanced dataset? At the very least, you need people at your company who know this answer for when the 3rd parties report their “outstanding results”.

Hire a Chief Artificial Intelligence Officer(CAIO) or a Chief Algorithmic Underwriting Officer (CAUO)- Yes I’m talking my own book, but both these positions will become more prevalent at (re)insurance companies. This function should not live under your IT department umbrella. The future of underwriting will be bionic, and look a lot more like the current mix of fundamental and quantitative trading in finance and at multi-manager, multi-strat hedge funds.

Form a multidisciplinary AI regulatory group - have a plan for the coming regulation. Prepare for initial governmental regulatory overreach. The relative differences so far in the US vs European approach to AI regulation show that Europe’s “too much” leads to an AI innovation exodus. Draconian approach to regulation? No problem, you can’t use our large language models in your country.

Make the use of AI and LLM tools part of yearly reviews- The more people comfortable using the tools, the more muted the coming shock. What gets measured gets done. Encourage a forcing function.

Image if you will for a moment Steve Ballmer is a (Re)insurance company “old school, way it’s always been done” executive talking about the new AI tech coming out:

“What was your reaction when you saw the iPhone coming out?”

Double click to interact with the video:

Now take this line:

“We have our strategy. We’ve got great Windows mobile devices in the market”

Translated to (Re)Insurance:

“We have our strategy. We’ve got great [insert way it’s always been done here] in the market.”

Yes I’m cherry picking to make a point, and I heard that Steve Ballmer wound up doing okay after all (go Clippers!), but start thinking and prepping.

Survival preppers think about a future in which they have to prepare for when the shit hits the fan (SHTF), an initial stage leading to the end of the world as we know it (TEOTWAWKI). Preppers love acronyms.

I am okay with being a paranoid AIEOTIW(Artificial Intelligence End of the Insurance World) prepper .

After all, paranoia plus preparation is a put option, a time well spent mental puzzle, and a form of…yes, insurance.

Get going.

Don’t slow down.

Great read. Really boils down to a decision of when insurers will seriously invest and operationalize this AI focus. It will happen, but companies will get the timing wrong and that will cause the pain. Either too early and board/employees complain or too late and miss the boat. Who plays the hand well

...get your 🍿 ready!